Let’s learn how we can help you manage your credit.

What is a credit score?

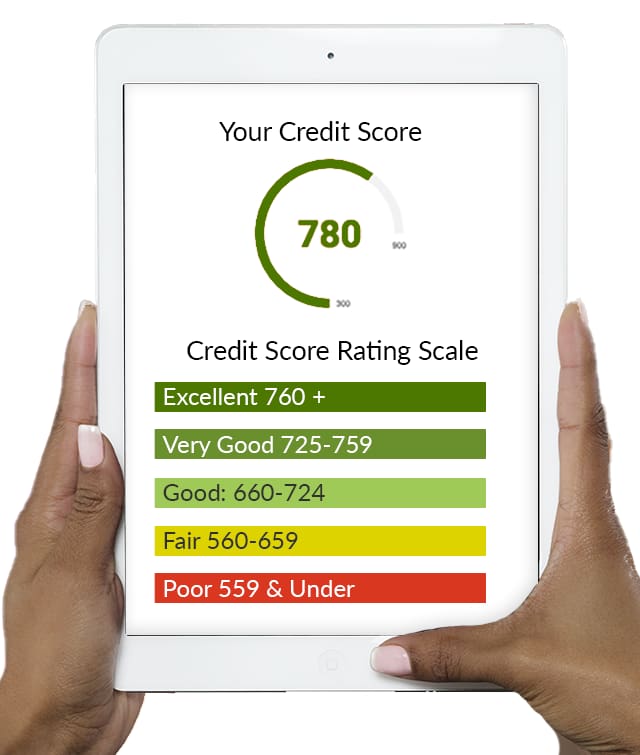

Your credit score is a number showing how well you manage credit.

It’s a scale between 300-900 points and based off your credit report.

For a copy of your credit report, visit TransUnion or Equifax. Additional fees may apply.

Why credit score matters

Your credit score impacts many important decisions, including:

Getting approved for a credit card or loan

Getting approved for buying or renting a home

Qualifying for a lower interest rate

Getting hired for certain jobs

Accessing a higher credit limit or loan/mortgage amount

Determining your insurance premiums (in some provinces)

As permitted by law for certain products in certain jurisdictions

What is a Credit Report?

A credit report provides a summary of your credit history with credit cards, loans and mortgages.

Companies including your bank, credit card, and telecommunications companies submit information to the credit bureau to show how you manage credit.

The information submitted includes things such as:

When you opened your account(s)

How much money you owe

Whether you’ve made your payments on time

Whether you’ve missed payments

Whether you’ve gone over your limit

How to improve your credit score:

Keep your accounts up-to-date and in good standing

Make payments on time and always pay at least the minimum payment by the due date

Only spend what you can afford to pay off monthly

Remember:

If you ever have trouble making your payments, you should reach out to your lender(s) and let them know. They may have programs that can help you.

Update your address and email to ensure you receive your statements.

How can we help manage your account?

Online Account

Access and manage your account online, anytime and anywhere

Your payment history can be an important factor in your credit score. It helps lenders predict whether they can count on you to pay back the money they lend you.

Your payment history includes every time you make a payment or miss a payment on your credit card, line of credit, mortgage, or cell phone bill. This information is reported to credit agencies to help them determine your credit score.

Use of available credit

Lenders look at how much you owe and the total per cent of your available credit. It helps them determine whether you can manage more payments. So, if you’re always close to maxing out your credit cards or line of credit, it makes you a higher risk to lenders.

Length of credit history

If you have a long-time credit history, it gives lenders a more accurate picture about how you use credit. If you are new to credit, it is harder for lenders to predict how you use credit. As a result, you may have a harder time getting approved for credit or get a higher interest rate.

Number of credit inquiries

If you frequently apply for new credit it may not reflect well on your credit score. Your score will consider the number of times your credit has been checked in the last five years, the number of credit accounts you have recently opened.

Types of credit you have

If you have different types of credit it may show lenders how well, you manage your credit overall and could help your credit score. However, it is important to be responsible with how much credit you have, keeping it at a manageable amount for your current financial situation.